Learning Center

How to fit an interest rate model and simulate random interest rates?

SAFE TOOLBOXES® comes with many types of models to deal with interest rates. They are presented in the table below:

| Model | Objective |

|---|---|

Vasicek |

Models the evolution of short-term interest rates. |

CIR (Cox–Ingersoll–Ross) |

Models the evolution of short-term interest rates. |

Svensson |

Models the full yield curve from market data. |

Nelson and Siegel |

Models the full yield curve from market data. |

HJM (Heath-Jarrow-Morton) |

Models the full yield curve from market data and its evolution over time. |

Cubic spline |

Interpolate over some set of yield nodes already calculated using any yield curve construction method. |

Flat forward |

Interpolate over some set of yield nodes already calculated using any yield curve construction method. |

All above functions follow a very convenient syntax in their name definitions. They all begin with “sInterestRates_” followed by the name of the model and an end that has the following meaning:

- FIT: Get the parameters of the model from data.

- RAND: Returns a random yield or random curve.

- SpotYield: Returns the yield that discounts the cash flow at time t to the present time.

- PriceZeroCouponBond: Returns the discounting factor the cash flow at time t to the present time.

- PRICES: Returns the prices of a list of fixed income instruments.

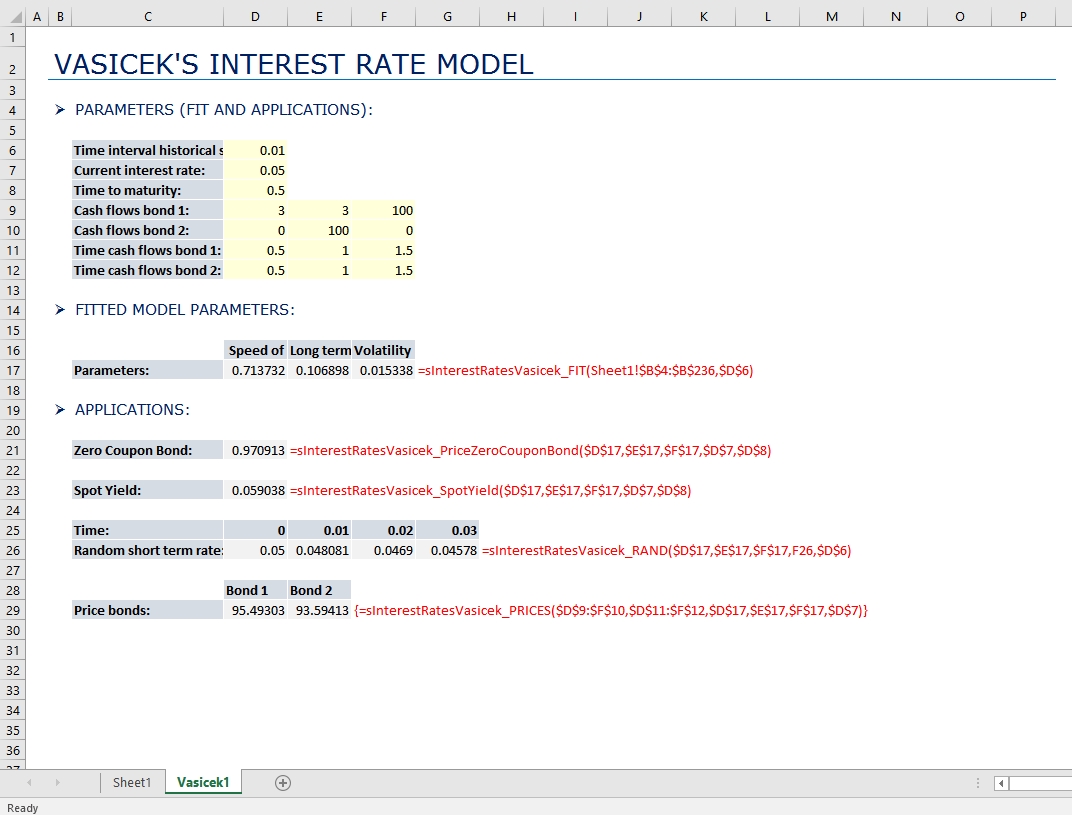

Let’s illustrate all these functionalities using the Vasicek model as an example. The fitting inputs for this model is a list of historical short-term interest rates, as the ones shown below:

A |

B |

C |

D |

|

1 |

Historical short term interest rates |

|

|

|

2 |

|

|

|

|

3 |

Time |

Rate |

|

|

4 |

0 |

0.055 |

|

|

5 |

0.01 |

0.054649 |

|

|

6 |

0.02 |

0.052634 |

|

|

7 |

0.03 |

0.052038 |

|

|

8 |

0.04 |

0.050721 |

|

|

9 |

0.05 |

0.051034 |

|

|

10 |

0.06 |

0.050217 |

|

|

11 |

0.07 |

0.050458 |

|

|

12 |

0.08 |

0.050591 |

|

|

13 |

0.09 |

0.049645 |

|

|

14 |

0.1 |

0.052252 |

|

|

... |

... |

... |

... |

... |

223 |

2.19 |

0.090403 |

|

|

224 |

2.2 |

0.09004 |

|

|

225 |

2.21 |

0.089473 |

|

|

226 |

2.22 |

0.090949 |

|

|

227 |

2.23 |

0.094295 |

|

|

228 |

2.24 |

0.096013 |

|

|

229 |

2.25 |

0.09709 |

|

|

230 |

2.26 |

0.097574 |

|

|

231 |

2.27 |

0.09818 |

|

|

232 |

2.28 |

0.098084 |

|

|

233 |

2.29 |

0.095937 |

|

|

234 |

2.3 |

0.092375 |

|

|

235 |

2.31 |

0.091961 |

|

|

236 |

2.32 |

0.092919 |

|

|

237 |

|

|

|

|

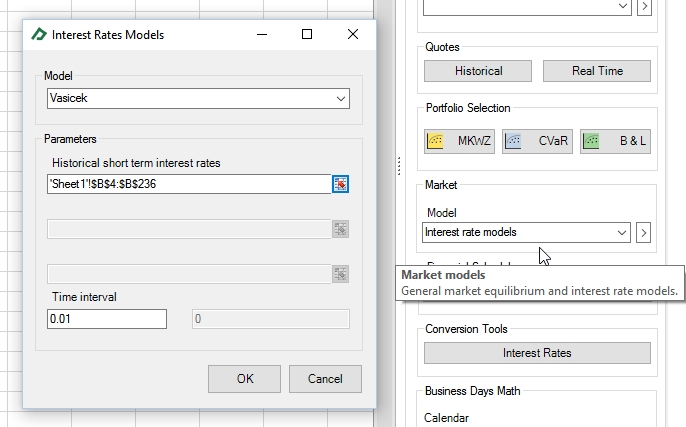

To fit the model, at the Financial Toolbox tab select the option “Interest rate models” in the “Market” group. Then fill the fields as following:

After confirming, a new sheet will appear with the fitted parameters for the model and some sample applications that you can quickly adapt to calculate something that you want.